If you work in affordable housing, 2026 LIHTC Income Calculation just got a lot more important. A payroll change tied to the One Big Beautiful Bill Act is already changing what you see on paystubs.

That matters because 2026 LIHTC Income Calculation depends on correct income, not just taxable wages. If your staff uses the wrong line on a paystub, the file can be wrong from day one.

And that is the kind of mistake that sneaks in quietly. No loud warning, no flashing sign, just a file that looks fine until someone checks the math during compliance monitoring.

For property management teams, this is where real risk lives. A line marked nontaxable may still count as income for eligibility at LIHTC properties.

That sounds backward at first. But payroll tax treatment and housing tax credit rules do not always match.

The big issue for 2026 is overtime. Employers are now breaking out the part of overtime pay that is deductible for federal tax purposes.

Some paystubs will show that amount as nontaxable overtime, qualified overtime, or something close to that. If your team reads only taxable gross income, household income can be undercalculated.

And undercounted income is not a small clerical issue. It can put a file out of compliance and create problems under a regulatory agreement or other program requirements.

Juanita Jeanie Sanchez of Sanchez Compliance & Consulting has spent more than 29 years helping owners, agents, and management teams fix this kind of problem before it grows. Her work centers on file reviews, audit prep, utility allowance support, first-year review help, and the backup your team needs when the pressure is on.

Her approach is simple. Stay audit-ready, because a calm audit season starts months before anyone asks for the file.

Table Of Contents:

- Why this search needs a beginner guide

- What changed under the One Big Beautiful Bill Act

- 2026 LIHTC Income Calculation and the paystub trap

- What qualified overtime actually means

- How to review a paystub in 2026 without missing income

- The difference between nontaxable paystubs and non countable income

- Allowance or reimbursement

- Why Box 12 Code TT matters so much

- A simple example your team can use

- What about state overtime rules or union overtime

- What OBBBA overtime rules mean for site teams

- Best practices for property management companies

- Why experienced file review matters more now

- The law is temporary, but the risk is here now

- How to keep files audit-ready in 2026

- Conclusion

Why this search needs a beginner guide

If someone searches “2026 LIHTC Income Calculation”, they are usually trying to solve a real work problem. They are not looking for theory.

They want to know what changed, what counts, and what to do with the paystub in front of them. They may also be trying to line up income limits, rent limits, and household eligibility without slowing down site operations.

That is why a beginner guide is the best fit here. It gives your site room to explain the new payroll treatment in plain US English and then show staff how to review income without guessing.

And this topic needs that kind of clarity. A lot of housing professionals are seeing these payroll lines for the first time, even if they already know HUD data, HUD income rules, or are implementing the new 2026 income and rent limits.

What changed under the One Big Beautiful Bill Act

The One Big Beautiful Bill Act, often shortened to OBBBA, became law on July 4, 2025. One part of the law created a federal tax deduction for certain overtime pay.

The deduction is often called, “no tax on overtime”, but that label can fool people. It does not mean all overtime disappears for income calculations in the LIHTC program.

It means certain overtime premium amounts get different tax treatment for federal reporting. Payroll systems are now reflecting that change in new ways.

The IRS explained this reporting change in its overtime reporting guidance. Starting in 2026, employers must report qualified overtime compensation separately on the employee Form W-2 using Box 12 Code TT.

That code matters a lot. It creates a trail you can compare against year-to-date totals, paystub entries, and other records used to confirm correct income.

For teams that already work with an income limit calculator, limit calculator tools, or HUD user resources, this is a reminder that wage reporting changes can affect file review even when income limits stay the same. Countable income and income limit questions are related, but they are not the same task.

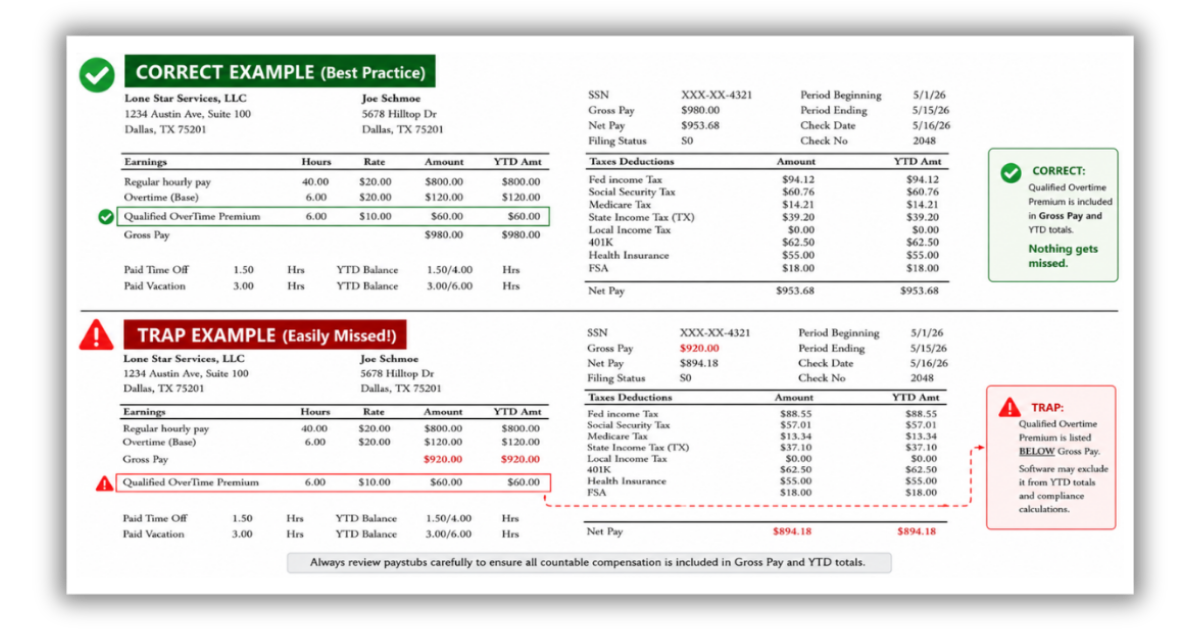

2026 LIHTC Income Calculation and the paystub trap

Here is where teams can get tripped up. A paystub may now separate out a piece of overtime into its own tracking line, causing confusion if a reviewer looks only at standard gross wage lines.

If a compliance reviewer grabs only taxable gross income, the annualized income can come out too low. The resident did earn that overtime pay, even if payroll labels part of it differently for tax reasons.

This is the trap. Nontaxable on a paystub does not automatically mean excluded from housing income or low-income housing tax credit eligibility.

And this trap will catch busy staff members first. They are trying to move fast, finish files, and trust the software.

But payroll software is not your compliance manual. It is just a tool, and it does not replace LIHTC compliance training, regulatory agreements, or your housing agency guidance.

What qualified overtime actually means

Qualified overtime is not the full overtime rate. It is only the premium part, which is the extra half in time-and-a-half.

Here is the easy way to see it. If an employee earns $20 an hour and overtime is paid at $30 an hour, the extra $10 is the premium.

That $10 is the amount treated as qualified overtime for federal tax deduction rules. But for LIHTC income review, the full $30 still matters as earned income.

That split is the whole story in one sentence. Tax treatment changed, but countable income did not change with it.

The Fair Labor Standards Act sets the federal overtime framework that drives this tax deduction rule. The FLSA overview from the U.S. Department of Labor is helpful if your team wants the labor law side.

This matters for more than just tax credit files. Staff who also work with public housing, rural development, trust fund, housing trust fund, or other financing programs can run into similar confusion if they assume tax treatment and program income treatment are always the same.

How to review a paystub in 2026 without missing income

You do not need a brand-new process. But you do need a sharper one.

Use this review method each time overtime shows up on a paystub. It is simple, and it catches the problem early.

- Read every pay line, not just taxable gross.

- Look for labels like nontaxable OT, qualified OT, overtime premium, or similar terms.

- Ensure any isolated overtime premium lines are fully included in your annualized gross income calculation, even if listed under a separate payroll tracking code.

- Check if flat monthly payments appear anywhere else on the stub.

- Verify with the employer if a recurring payment is an allowance or a reimbursement.

This process is not fancy. But it works because it slows down the exact place where errors start.

It also helps to keep a note in the file that explains which line was used for annualizing income. That is useful during compliance monitoring, investor review, and internal quality control.

For properties that also track rent limit and rent levels against current income limits, a bad income calculation can trigger the wrong unit designation or tenant selection decision. One wrong number can create more than one problem.

The difference between nontaxable paystubs and non countable income

This point deserves its own section because it causes so much confusion. Payroll language and compliance language often sound alike, but they do different jobs.

Taxable means taxed. Countable means included for eligibility.

Those are not the same test. And if your staff treats them as the same, your annual income math can go sideways.

A nontaxable paystub item might still count as income. That includes qualified overtime deductions that payroll systems carve out for tax reasons.

So train your team to pause when they see the words nontaxable. Those two words should spark a second look, not a quick pass.

This is especially important in low-income housing and income housing tax credit files where staff may already be juggling median income charts, area median figures, and unit designations. A simple label can lead reviewers in the wrong direction.

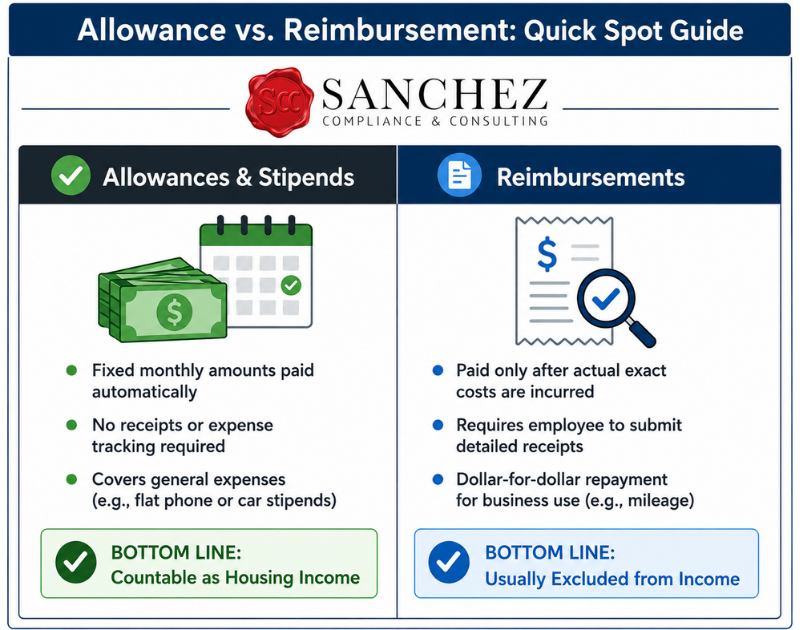

Allowance or reimbursement

This is another area where files get messy. And yes, it still trips people up year after year.

If an employee gets a flat amount every month for something like phone or internet, that payment is often an allowance. That usually means it counts as income.

If the employer repays an actual expense after getting a receipt, that is usually a reimbursement. That type of payment is generally excluded.

The difference sounds small. In file review, it is huge.

A quick way to spot the difference

| Payment Type | How It Works | Likely Treatment |

|---|---|---|

| Flat phone stipend | Employee gets $75 each month no matter the bill. | Count as income. |

| Receipt-based phone repayment | Employer repays part of actual bill after review. | Usually excluded. |

| Car allowance | Fixed monthly amount paid each pay period. | Count as income. |

| Mileage reimbursement | Paid after actual business miles are documented. | Usually excluded. |

| Internet stipend | Same amount paid every month with no receipt needed. | Count as income. |

| Travel repayment | Paid only after actual costs are submitted. | Usually excluded. |

Never assume a flat rate is a reimbursement. If it stays the same month after month, treat it like a question mark until you verify the exact details with the employer. This is where clarifying with the employer truly matters. When obtaining third-party verification, compliance teams must explicitly ask the employer whether the recurring payment is an unconditional allowance or a strict, receipt-backed expense reimbursement. If the employer confirms it is an allowance, it must be counted toward the household’s annualized income.

This point can also affect households near an income limit. A recurring stipend that gets missed may push a household above a project income limit, even if the initial file looked fine.

Why Box 12 Code TT matters so much

Starting with 2026 Forms W-2, employers must report qualified overtime compensation in Box 12 with Code TT. This is one of the best audit trails you will have.

If you see a Code TT amount, it tells you qualified overtime existed during the year. That should prompt you to review paystubs and year-to-date wages with care.

Did the paystub taxable totals leave that premium out? Did the annualized math pick up the full amount earned?

Those are the questions to ask. You want answers before someone else asks them first.

The IRS also gave transition relief for early implementation issues in its transition guidance. That helps explain why current payroll records may look inconsistent as employers catch up.

For teams that compare multiple records during file review, Code TT can help explain why W-2 wages and paycheck totals do not line up the way they did in prior years. And while we do not typically see or use W-2 forms for current documentation of income, it is good to know about this TT code so we do not inadvertently miss the countable income. That kind of mismatch is exactly what triggers deeper review during LIHTC compliance testing.

A simple example your team can use

Say an employee earns $18 per hour. They worked 80 regular hours and 10 overtime hours in the pay period.

Regular wages are $1,440. Overtime at time-and-a-half is $270, which means the premium piece is $90.

Some payroll systems may show taxable gross that leaves out the $90 premium because it gets different federal tax treatment. If your staff annualizes from that taxable line only, income will be short by $90 for the period.

That may not sound like much at first glance. But stretch it over the year and now the file tells the wrong story.

That is why 2026 LIHTC Income Calculation needs a full pay review, not a skim. Small misses stack up fast.

| Item | Amount |

|---|---|

| Regular pay | $1,440 |

| Total overtime pay | $270 |

| Qualified overtime premium | $90 |

| Possible amount missed if staff uses taxable wages only | $90 |

In projects receiving tax-exempt bond financing or other housing tax programs, the review approach may differ by program rules. Even so, the core lesson stays the same: read the whole paystub before you annualize anything.

What about state overtime rules or union overtime

This part matters for payroll understanding. Some overtime paid under state law or a union contract may not meet the federal standard used for the tax deduction.

So the word overtime on a check does not always mean qualified overtime for Code TT reporting. That is one more reason not to guess.

The tax team at KPMG published a helpful write-up on overtime and tip deduction rules under the new law. It gives useful context on reclassification risk and why payroll labels may not tell the full story.

That distinction matters to housing professionals working across states. State wage rules may differ, but your file still needs the correct income calculation for the program in front of you.

What OBBBA overtime rules mean for site teams

You do not need everyone on your team to become a payroll expert. But your reviewers do need a clean checklist.

Train them to slow down at three spots. Taxable gross, flat recurring payments, and any line with overtime wording.

That is where most 2026 file issues will start. Not in some strange corner case, but in routine payroll review.

It also helps to flag resident files with variable work hours for a second review. Overtime-heavy households carry more risk now because the paystub layout itself can hide part of the earnings.

If your company uses software tied to income limit calculators, rent limit calculators, or imported HUD published data, remind staff that these systems do not confirm countable earnings for them. The software can support the process, but it does not hold sole responsibility for the result.

Best practices for property management companies

If you manage affordable communities, your process needs to work at scale. It has to be repeatable, teachable, and easy to check.

These steps are practical and worth putting into your policy notes.

- Update income review checklists to mention qualified overtime and Code TT.

- Train staff not to rely only on gross taxable income lines.

- Ask employers to explain recurring stipends and fixed payments.

- Keep verification notes clear and consistent in every file.

- Run second reviews on overtime-heavy households.

- Compare annual wage records against file calculations before audit season.

- Review current income limits and rent limits with staff at the same time.

That last point matters a lot. File errors feel very different when you catch them in house instead of during an audit.

It is also smart to keep a short training memo with examples from your own files. Real examples help staff remember how to separate taxable wages from countable income.

Why experienced file review matters more now

There is a reason payroll changes create so much trouble in compliance. They look harmless until you compare documents side by side.

One line on a paystub says nontaxable. Another report shows year-to-date wages. A later W-2 shows Code TT.

If no one connects those dots, the wrong income ends up in the file. That can affect tax credits, owner reporting, and property performance under the low-income housing tax credit program.

This is exactly where Sanchez Compliance & Consulting helps. Jeanie works with management agents, owners, developers, investors, compliance teams, regional managers, and site staff who need a solid second review.

Her firm supports file review process improvement, backup for busy teams, first-year review help, audit prep, due diligence reviews, and utility allowance work. The focus stays the same every time: reduce stress, build staff understanding, and cut the risk of noncompliance before it gets expensive.

Sanchez Compliance & Consulting is also backed by long-standing business certifications, including WBENC, WOSB, Texas HUB, and MWBE. That matters to many partners who need an experienced and dependable compliance resource in affordable real estate.

The law is temporary, but the risk is here now

The overtime deduction under OBBBA is temporary under current law. It is set to expire on December 31, 2028.

There are also income phaseouts and deduction caps written into the law. The deduction begins to phase out above $150,000 for individuals and $300,000 for joint filers (fully phasing out at $275,000 and $550,000)—though any applicant reaching these income levels would already far exceed LIHTC eligibility limits.

You can review the larger bill picture through the bill summary on Congress.gov. That broader view helps explain why payroll departments are making updates now.

But your team should not wait for perfect uniformity in paystubs. The reporting change is already in motion, and the file review risk is already here.

That is true whether your property follows standard LIHTC rules, layered financing rules, housing trust requirements, or held harmless limits tied to prior income limits hold harmless policies. Payroll confusion does not wait for your next annual training.

How to keep files audit-ready in 2026

If you want a short answer, it is this: review income like the paystub may be hiding something.

That may sound a little cynical, but it is practical. Systems change faster than training, and payroll labels can mislead even careful staff.

Keep your files clean with habits that hold up under pressure.

- Use third-party verification when payroll labels are unclear.

- Read all pay lines and not just the taxable box.

- Compare paystub math to annual records once available.

- Document why a stipend was counted or excluded.

- Send high-risk files for a second review before audit time.

- Check whether updated income limits or rent levels affect next steps.

That is how you stay steady. Slow, clear, repeatable file work wins this game.

It also helps to watch for new HUD published releases, press releases from allocating agencies, and annual updates from your housing agency. Those items may not change this overtime rule, but they often affect income limits, rent limit updates, MTSP income tables, fair market assumptions, and related program requirements.

For mixed-finance sites, bond deals, or projects receiving layered subsidies, keep one written process that explains who reviews payroll income, who checks income limits, and who signs off before move-in. That keeps accountability clear and reduces file drift.

Conclusion

2026 LIHTC Income Calculation is no longer just about reading gross wages and moving on. The new overtime tax treatment under OBBBA means property management teams must review paystubs with more care, especially where qualified overtime, nontaxable pay items, and fixed allowances appear.

If your staff misses those details, household income can be undercounted, and the file can drift out of compliance. A sharp review process, strong third-party verification, and a second set of eyes can make all the difference.

Put it all together and the message is simple. Countable income, income limits, rent limits, and file documentation all work best when staff read the full pay record and confirm the details instead of relying on one wage line.

If your team wants support before audit season gets hectic, Sanchez Compliance & Consulting can help you review files, train staff, and stay ready all year. That is the real goal behind better 2026 LIHTC Income Calculation work: fewer surprises, less stress, and stronger files.